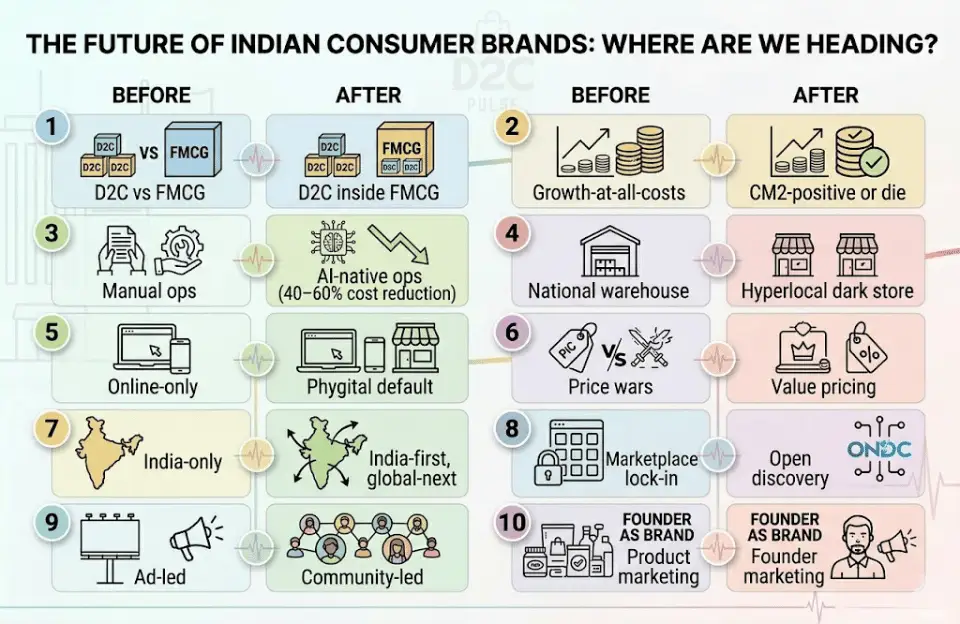

The Future of Indian Consumer Brands: 10 Forces That Will Shape the Next Decade

FMCG Giants Are Buying D2C. AI Is Replacing Ad Agencies. Quick Commerce Is the New Shelf. And Only Profitable Brands Survive. Here Is What the Future of Indian Consumer Brands Looks Like.

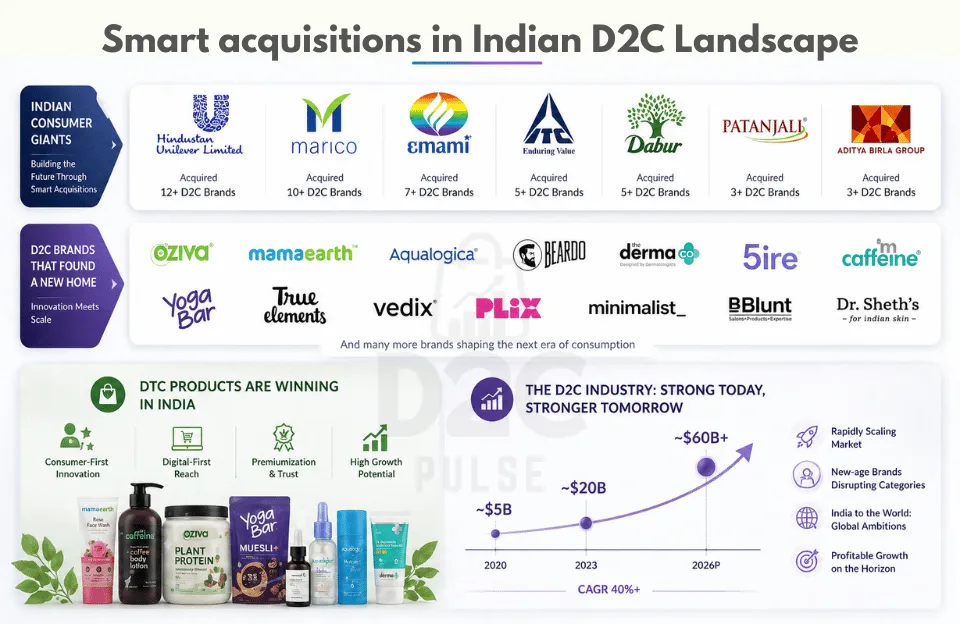

The future of Indian consumer brands is being written now. Not in five years, Now! In 2025, HUL paid Rs 2,955 crore for Minimalist. Marico bought Just Herbs, Plix, True Elements, and Beardo. ITC acquired Yoga Bar and Prasuma. Emami took full control of The Man Company. Two-thirds of FMCG acquisitions between FY21 and FY25 were in the D2C space.

At the same time, quick commerce grew at 75% year-on-year. ONDC expanded to 630+ cities. AI tools cut content creation costs by 60–70%. D2C brands leased 18% of retail space. The India D2C market crossed $108 billion. And 250 million Indians now shop directly from brands.

The future of Indian consumer brands will not look like the past five years. The era of growth-at-all-costs is over. The time of cheap Meta ads is over. The years of raising capital without positive unit economics are over. What comes next is a market that rewards brand depth, operational discipline, and the ability to build across channels.

This article maps the 10 forces that will shape the future of Indian consumer brands over the next decade. Each force is already visible, backed by data and separate the brands that survive from the brands that do not.

Force 1: FMCG-D2C Consolidation Will Reshape the Future of Indian Consumer Brands

The biggest structural shift in the future of Indian consumer brands is the merger of D2C and FMCG. It has already started. HUL bought Minimalist for Rs 2,955 crore. Marico bought Beardo, Just Herbs, Plix, and True Elements. ITC bought Yoga Bar. Emami took full ownership of The Man Company. Nykaa acquired Dot & Key. Reliance acquired a stake in Ed-a-Mamma.

This is not slowing down. Two-thirds of FMCG acquisitions from FY21 to FY25 were D2C brands. The logic is simple. FMCG giants have distribution, cash, and scale. D2C brands have digital-first customers, product innovation, and brand loyalty with young consumers. The marriage makes both stronger.

For the future of Indian consumer brands, this means three things. First, the best D2C brands will be acquired. If you build a Rs 300–500 crore brand with 60%+ gross margins and strong repeat rates, FMCG companies will pay 5–10x revenue for it. Second, D2C brands that cannot be acquired (low margins, no moat, no repeat) will die. Third, FMCG companies that do not acquire D2C will lose relevance with millennial and Gen Z consumers.

Also Read: Why Investors Love D2C Brands in India for the full FMCG acquisition deal table

Force 2: The Profitability Pivot Is Non-Negotiable

The future of Indian consumer brands belongs to profitable brands. Full stop. The funding winter of 2023–2024 forced every D2C brand to care about unit economics. Investors now screen for positive CM2 before writing a cheque. Valuations have compressed from 10–15x revenue to 2–4x. Series A rounds demand $5–10 million in ARR with a path to profitability.

The brands that survived: boAt posted Rs 60 crore net profit in FY25. Lenskart posted Rs 297 crore net profit. Minimalist was profitable before HUL acquired it. The brands that did not survive: Good Glamm wrote down $221 million. 10Club shut down after raising $40 million. Multiple roll-up models collapsed.

In the future of Indian consumer brands, revenue without margin is a death sentence. The winners will track CM2 by channel, achieve EBITDA breakeven within 24–36 months, and build brand assets that reduce CAC over time.

Also Read: Achieving Profitability in D2C for the 5-stage framework

Force 3: AI Will Change How the Future of Indian Consumer Brands Operates

AI is not coming to consumer brands. It is already here. AI-generated ad creatives cut design costs by 60–70%. AI chatbots handle customer support at Rs 2–5 per interaction instead of Rs 20–30. AI-powered product recommendations increase AOV by 15–25%. AI demand forecasting reduces dead inventory by 20–30%. And AI search engines like ChatGPT, Perplexity, and Google AI Overviews are becoming product discovery channels.

For the future of Indian consumer brands, AI changes three things. First, content creation becomes near-free. A brand that spent Rs 5 lakh per month on creative can now spend Rs 50,000 with AI tools. Second, customer support scales without headcount. Third, product discovery shifts from search engines to AI agents. Brands that build structured content, reviews, and product data get recommended by AI. Brands that only run ads do not.

HUL is already using AI for geo-targeted product assortment. ITC uses AI for nutrition customisation. The future of Indian consumer brands will be AI-native. Not AI-aware. AI-native. The brands that embed AI into operations from day one will operate at 40–60% lower costs than those that do not.

Force 4: Quick Commerce Becomes a Core Channel

Quick commerce grew at 75% year-on-year. The market hit Rs 11,000 crore monthly GMV by 2026. Non-grocery categories are growing 1.6x faster than groceries. Blinkit, Zepto, and Swiggy Instamart now deliver fashion, beauty, and electronics in 10–30 minutes. D2C brands are shifting from national warehouses to hyperlocal dark stores.

For the future of Indian consumer brands, quick commerce changes the distribution playbook. The shelf is no longer a retail store. It is a dark store 3 kilometres from the customer. Brands that win placement on Blinkit and Zepto get impulse purchases that offline stores cannot match. But the trade-off is real: 30–40% commissions. Only high-margin, high-velocity SKUs work on quick commerce.

The future of Indian consumer brands includes a quick commerce strategy for every brand above Rs 10 crore revenue. Not as the primary channel. As the trial and impulse channel that feeds your D2C website and offline stores.

Force 5: Omnichannel Becomes the Default for the Future of Indian Consumer Brands

D2C brands leased 6 lakh square feet of retail space in H1 2025. That is 18% of total retail leasing, up from 8% the year before. Lenskart has 2,700+ stores. Mamaearth is in 40,000+ outlets. Nykaa has 250+ stores. Sugar Cosmetics expanded to offline counters across India.

The future of Indian consumer brands is not online-only. It is not offline-only. It is omnichannel by default. The winning model: build the brand online first. Prove unit economics. Collect first-party data. Then expand offline where it adds value. Stores become experience centres, return hubs, and brand-building tools. Not just sales points.

AR-mediated experiences like virtual try-ons deliver 94% higher conversion than traditional images. Phygital (physical + digital) is the operating model. The future of Indian consumer brands treats every channel as connected. A customer discovers on Instagram, researches on the website, tries in-store, and reorders on WhatsApp. The brand that owns all four touchpoints wins.

Also Read: The Shift from Offline to Digital-First for the full omnichannel playbook

Force 6: Premiumization Drives Margin Expansion

30% of FMCG sales now come from premium products. 60% of car sales are SUVs. Specialty coffee outsells instant in urban metros. The future of Indian consumer brands is premium. Not luxury. Premium. Consumers are paying more for quality, transparency, and identity.

For the future of Indian consumer brands, premiumization means higher AOV, better gross margins, and stronger brand loyalty. Minimalist sells serums at Rs 500–700. Blue Tokai sells coffee at Rs 500–800. Mokobara sells bags at Rs 5,000–15,000. These brands are profitable because premium pricing gives them margin to invest in brand, content, and experience.

The brands that race to the bottom on price will die. The future of Indian consumer brands belongs to those that price for value and justify it through education, transparency, and product quality.

Also Read: Rise of Premiumization in India for the 7 forces and 8-category breakdown

Force 7: Cross-Border Expansion Opens New Growth Lanes

Digitally-born exports from India were worth $4.7 billion in 2024. By 2030, they are projected to reach $22 billion. The future of Indian consumer brands is not India-only. It is India-first, global-next.

Lenskart has 27 stores across the GCC. iD Fresh Food earns 25% of revenue from the Middle East. Plum sells in 15 countries. Wakefit launched in the UAE. Bombay Shaving Company operates in 5 international markets. The pattern: prove in India. Scale abroad. The UAE, Southeast Asia, and the US are the three priority markets.

The future of Indian consumer brands includes a cross-border strategy at Rs 25 crore revenue, not Rs 100 crore. New markets. New customers. Better unit economics. Lower competition. Indian products (Ayurveda, clean beauty, ethnic food) carry a structural advantage globally.

Also Read: Cross-Border Expansion Strategies for Indian D2C Brands for the market-by-market playbook

Force 8: ONDC and Open Commerce Reshape Discovery

ONDC is live in 630+ cities with 1.16 lakh+ sellers. Commissions are about 3%, compared to 15–30% on Amazon and Flipkart. The future of Indian consumer brands includes ONDC as a low-cost discovery channel. It will not replace Amazon. But it will give brands a way to reach new customers without paying 25% in marketplace fees.

For the future of Indian consumer brands, ONDC does what UPI did for payments: opens the network. Sellers list on any ONDC app. Buyers discover on any ONDC app. The protocol is open. No single company controls it. This is still early. But the trajectory is clear. Brands that list on ONDC today get first-mover advantage in a channel that will scale to hundreds of millions of orders.

Force 9: Community-Led Growth Replaces Ad-Led Growth

The future of Indian consumer brands will not be built on Meta ads alone. CAC has risen 30–40% year-on-year. 62% of founders report creative fatigue. The brands that cross Rs 100 crore do it with owned channels: WhatsApp communities, email lists, Instagram communities, and creator networks.

Sugar Cosmetics gets 50% of online revenue from its own website, driven by community loyalty. boAt built the boAtheads community. Whole Truth built a cult following around clean-label education. These brands do not depend on paid ads for every sale. They have audiences that buy because they belong.

The future of Indian consumer brands rewards community builders. A brand with 50,000 WhatsApp subscribers generates Rs 5–10 lakh per broadcast. A brand with zero community generates Rs 0 when ads stop.

Force 10: The Founder Becomes the Brand

Ghazal Alagh on Shark Tank India. Aman Gupta on Shark Tank India. Peyush Bansal on Shark Tank India. The founder is the most powerful marketing asset in the future of Indian consumer brands. A founder who explains why they started the brand builds trust that no ad can buy.

Minimalist’s founders (Mohit and Rahul Yadav) built credibility through ingredient transparency. Wakefit’s Ankit Garg built awareness through the Sleep Internship campaign. Whole Truth’s Shashank Mehta built trust through radical label transparency. Each founder became inseparable from the brand.

The future of Indian consumer brands demands founder visibility. Get on camera. Write on LinkedIn. Talk about why you built what you built. The founder story is the highest-converting piece of content. It is free. It compounds. And no competitor can copy it.

What the Future of Indian Consumer Brands Means for Each Player

| Player | What Changes | What to Do Now |

| D2C Founders | Profitability is mandatory. FMCG acquisition is a viable exit. AI cuts costs. Omnichannel is default. | Get CM2 positive. Build brand moat. Go omnichannel. Use AI tools. Plan cross-border at Rs 25 Cr. |

| FMCG Companies | D2C brands are eating young consumer share. Quick commerce is growing 3x faster than modern trade. | Acquire D2C brands. Build digital-first sub-brands. List on ONDC. Invest in AI personalisation. |

| Investors | Revenue multiples compressed. CM2 is the new screen. IPO pipeline includes boAt, Lenskart. | Back CM2-positive brands with Rs 50 Cr+ revenue. Focus on categories with repeat economics. |

| SaaS Companies | D2C tech stack spend is growing. AI tools replace manual work. Retention tools are in highest demand. | Build for retention (WhatsApp, email, loyalty). Integrate AI. Target Rs 30L–5Cr/mo D2C brands. |

| Agencies | AI cuts creative production costs 60–70%. Performance marketing alone does not work anymore. | Add brand strategy, CRO, and community building to your offering. AI-augment creative production. |

Key Takeaways

- The future of Indian consumer brands is being shaped by 10 forces right now. FMCG-D2C consolidation, profitability pivot, AI-native operations, quick commerce, omnichannel default, premiumization, cross-border expansion, ONDC, community-led growth, and founder as brand. Each is already visible. Each is backed by data.

- Consolidation is the defining structural shift. Two-thirds of FMCG acquisitions from FY21–FY25 were D2C brands. HUL bought Minimalist for Rs 2,955 Cr. Marico, ITC, Emami, and Nykaa all acquired D2C brands. The future of Indian consumer brands is D2C inside FMCG, not D2C versus FMCG.

- Profitability separates survivors from casualties. boAt: Rs 60 Cr profit. Lenskart: Rs 297 Cr profit. Minimalist: profitable pre-acquisition. Good Glamm: $221M write-down. The future of Indian consumer brands belongs to brands that make money, not brands that raise money.

- AI, quick commerce, and ONDC are the three infrastructure shifts. AI cuts operating costs 40–60%. Quick commerce is a Rs 11,000 Cr/month GMV channel growing at 75% YoY. ONDC offers 3% commission vs 15–30% on marketplaces. Each changes how brands operate, distribute, and grow.

- The winning formula for the future of Indian consumer brands: build premium products, achieve profitability early, use AI to operate lean, go omnichannel, expand cross-border, build community, and put the founder on camera. Simple to say. Hard to do. The brands that do all seven will be the ones worth Rs 1,000+ crore by 2030.

Frequently Asked Questions

What does the future of Indian consumer brands look like?

The future of Indian consumer brands is shaped by 10 forces: FMCG-D2C consolidation, the profitability pivot, AI-native operations, quick commerce as a core channel, omnichannel as default, premiumization, cross-border expansion, ONDC and open commerce, community-led growth, and the founder as brand. The market is moving toward profitable, omnichannel, AI-powered brands that operate across India and internationally.

Will FMCG companies keep buying D2C brands?

Yes. Two-thirds of FMCG acquisitions from FY21 to FY25 were D2C brands. HUL bought Minimalist for Rs 2,955 crore. Marico bought Beardo, Plix, Just Herbs, and True Elements. ITC bought Yoga Bar. The future of Indian consumer brands includes increased M&A as FMCG giants seek digital-first brands to reach younger consumers. D2C brands with Rs 300–500 crore revenue and strong margins are the most attractive targets.

How will AI change the future of Indian consumer brands?

AI will cut operating costs by 40–60%. Ad creative production drops from Rs 5 lakh to Rs 50,000. Customer support costs drop from Rs 20–30 to Rs 2–5 per interaction. AI-powered product recommendations lift AOV by 15–25%. And AI search engines become product discovery channels. Brands that build structured content and reviews get cited by AI. The future of Indian consumer brands will be AI-native, not AI-aware.

Is profitability now required for D2C brands in India?

Yes. The funding winter forced a profitability pivot. Investors screen for positive CM2 before investing. Valuations compressed from 10–15x revenue to 2–4x. The brands that survived (boAt, Lenskart, Minimalist) are all profitable. The brands that collapsed (Good Glamm, 10Club) were not. The future of Indian consumer brands belongs to those with positive unit economics, not those with the most funding.

What should D2C founders do now to prepare for the future?

Five things. First, get CM2 positive. It is the minimum threshold for survival. Second, build brand assets that reduce CAC: founder visibility, SEO content, community, and creator partnerships. Third, go omnichannel. Start with 1–5 stores or pop-ups. Fourth, use AI tools to cut operating costs. Fifth, plan cross-border expansion at Rs 25 crore revenue. The future of Indian consumer brands rewards brands that do all five. Not brands that do one well and ignore the rest.