D2C Funding Trends – India: What Changed, What’s Coming, and What Investors Want Now

A Complete Analysis of How D2C Funding Evolved from Boom to Correction to Discipline — and What 2026 Demands from Founders

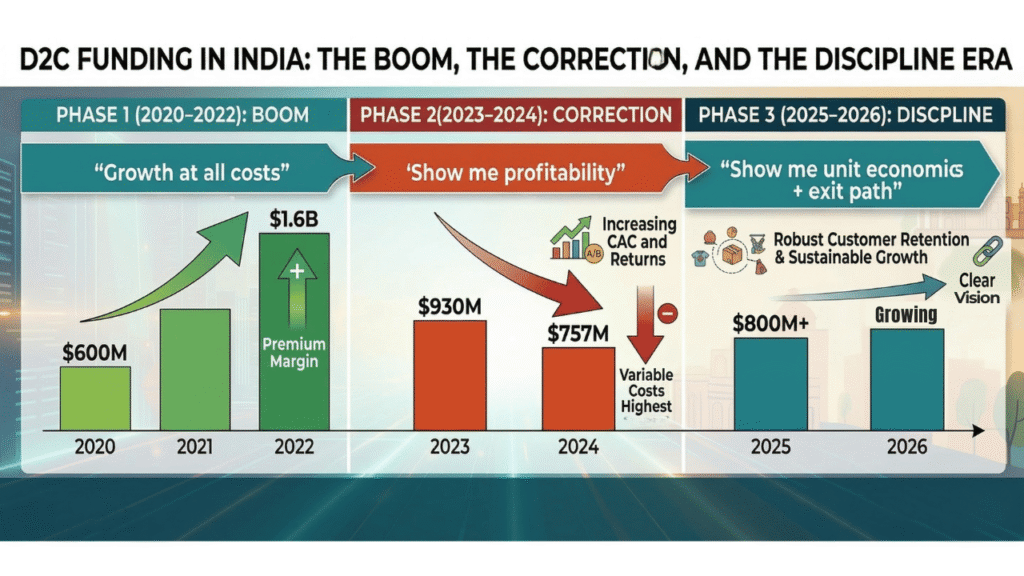

The story of D2C funding trends in India reads like a three-act drama. Act one was the boom. In 2021, global D2C funding hit $5 billion. Indian D2C startups raised $1.6 billion in 2022 alone. Valuations reached 10–15x revenue. Every brand with a Shopify store and an Instagram page was pitching for capital.

Act two was the correction. By 2024, D2C funding in India had dropped to $757 million — a 54% decline from 2022. Globally, D2C funding crashed 97% from its 2021 peak to just $130 million (excluding India). Unicorn creation stopped. Three IPOs happened in 2024, compared to six in 2023. Investors went quiet.

Act three is happening right now. It is the era of discipline. In 2025 and heading into 2026, D2C funding trends in India show a market that has sobered up but not shut down. Capital is flowing — but only to brands that demonstrate real profitability, strong unit economics, and a credible path to exit. The era of funding based on revenue growth alone is over.

This guide maps the complete arc of D2C funding trends in India. The data. The deals. The investor expectations. The categories attracting capital. The IPO pipeline. And — critically — what founders must demonstrate in 2026 to raise money in this new environment.

D2C Funding Trends in India: The Numbers That Tell the Full Story

Here is the funding journey for Indian D2C startups, year by year:

| Year | D2C Funding (India) | YoY Change | Unicorns Created | Key Signal |

| 2020 | ~$600M | — | 0 | COVID accelerates D2C adoption. Pandemic-driven demand. |

| 2021 | ~$1.2B | +100% | 2 | Peak hype. boAt and Licious become unicorns. |

| 2022 | $1.6B | +33% | 1 | All-time high. Valuations at 10–15x revenue. |

| 2023 | $930M | –42% | 0 | Correction begins. Investors demand profitability. |

| 2024 | $757M | –18% | 0 | Funding winter. Valuations compress to 2–4x revenue. |

| 2025 | Selective* | Stabilising | 0 | Discipline era. Fewer deals but larger cheques. |

| 2026 (so far) | Early signals positive* | Cautiously up | TBD | IPO pipeline. M&A rising. Profitability-first. |

*Note: 2025 full-year D2C-specific funding data is not yet consolidated as a single figure by major trackers. Overall Indian startup funding was approximately $10.5 billion in 2025, down 17% from 2024 (per Tracxn). D2C-specific funding is estimated to have remained in the $700M–$800M range based on disclosed deals. 2026 data reflects early Q1 signals only.

The pattern is clear. D2C funding trends in India peaked in 2022, corrected sharply in 2023–2024, and are now entering a phase where capital is available — but on fundamentally different terms.

India ranked as the second most funded country for D2C startups globally in 2024, behind the United States and ahead of China, the UK, and Italy (per Tracxn). The ecosystem is not dying. It is maturing. The rules of the game have changed.

What Changed: How D2C Funding Trends in India Shifted from Growth to Profitability

The shift in D2C funding trends in India can be summarised in one sentence: investors stopped rewarding revenue growth and started demanding contribution margin.

The Old Playbook (2020–2022)

- Raise capital. Spend on ads. Grow revenue at any cost.

- Valuations based on revenue multiples (10–15x).

- Profitability was a distant goal, not a near-term requirement.

- CAC was rising but nobody cared because funding was cheap.

- Angel tax exemption had not yet happened. Dilution was heavy.

The New Playbook (2025–2026)

- Investors screen for positive CM2 (contribution margin after marketing) before writing a cheque.

- Valuations have compressed to 2–4x revenue multiples.

- CAC payback periods under 6 months are expected. Under 3 months is ideal.

- Gross margins above 60% on core products are a baseline in most categories.

- Path to EBITDA positivity within 18–24 months is a standard ask.

- The Union Budget 2024 scrapped the angel tax on share premiums and reduced long-term capital gains tax on unlisted shares from 20% to 12.5%. This has made equity investing in D2C startups more attractive.

Praveen Govindu, a partner at Deloitte India, put it directly in a recent analysis (January 2026): brands can no longer rely on burning capital on quick commerce or paid channels. The focus is shifting from intent to execution. D2C funding trends in India now reward operational discipline, not pitch decks.

[Internal link: Read CAC vs LTV: The Unit Economics Deep Dive for the full framework investors use to evaluate D2C brands]

The Biggest D2C Funding Deals of 2025 and Early 2026

While the overall funding volume contracted, several brands raised significant rounds. These deals reveal where investor confidence is concentrated:

| Brand | Amount | Round | Year | Lead Investor(s) |

| GIVA (Jewellery) | Rs 530 Cr ($61.5M) | Series C | Jun 2025 | Creaegis, Premji Invest, Epiq Capital |

| The Whole Truth (Food) | $51M | Series D | Feb 2026 | Sauce.vc, Sofina, Peak XV, Z47 |

| Snitch (Fashion) | $40M | Series B | Jun 2025 | 360 ONE Asset, IvyCap Ventures |

| Farmley (Snacks) | $40M | Growth | 2025 | L Catterton, Fireside Ventures |

| Foxtale (Skincare) | $30M | Series B | Apr 2025 | Panthera Growth, Matrix Partners |

| Supertails (Pet Care) | $30M | Growth | Feb 2026 | Venturi Partners, Nippon India |

| Country Delight (F&B) | ~$25M | Growth | 2025 | Institutional round |

| Heads Up For Tails | ~$25M | Series B | 2025 | Apparel Group-linked strategic |

| Moxie Beauty (Haircare) | $15M | Series A | Dec 2025 | Bessemer, Fireside Ventures |

| Antinorm (BPC) | Rs 28 Cr | Seed | Jan 2026 | Fireside Ventures, V3 Ventures |

Two patterns emerge from this deal table. First, the investors are marquee names: Fireside Ventures, Premji Invest, Peak XV Partners (formerly Sequoia), L Catterton, and Bessemer. These are not speculative bets. They are conviction-driven investments in category leaders.

Second, the categories getting funded are the ones with strong repeat consumption and clear unit economics: jewellery, food, beauty, pet care, and fashion with proven profitability. Hardware and general lifestyle brands are conspicuously absent from the large-deal list.

Marmeto, India’s First Shopify Premier Partner, Pivots From Services to Product-First Technology Company

Anveshan and the Rs 1,000 Crore Farm-to-Fork Valuation Leap

L’Oréal in Talks to Acquire D2C Beauty Startup Innovist

Assiduus Global Raises $25 Million to Scale AI-Powered Middleware for Cross-Border D2C Commerce

The D2C Startup Mafia: How Second-Time Founders are Securing 2026 Funding

Bidso Raises Rs 63 Crore Series A Led by Blume Ventures to Scale Contract Manufacturing Platform for D2C Brands

Where the Money Is Going: D2C Funding Trends by Category

Not all D2C categories attract equal investor interest. The D2C funding trends in India show clear category preferences:

Hot Categories (Attracting Concentrated Capital in 2025–2026)

- Beauty and skincare. Foxtale ($30M), Moxie ($15M), Antinorm (Rs 28 Cr seed). HUL’s Rs 2,955 Cr acquisition of Minimalist signals that even legacy giants are buying into D2C beauty.

- Jewellery. GIVA’s Rs 530 Cr round was one of the largest pure D2C rounds in 2025. BlueStone IPO’d in August 2025 with Rs 1,770 Cr revenue. Palmonas raised Rs 55 Cr in Series A.

- Food and beverages. The Whole Truth ($51M), Farmley ($40M), Country Delight ($25M). Subscription-driven, repeat-heavy food brands are investor favourites.

- Pet care. Supertails ($30M in Feb 2026), Heads Up For Tails ($25M). $124M in cumulative pet care startup funding across 64 rounds between 2022 and November 2025.

Cooling Categories (Less Funding Activity)

- Audio and wearables. boAt is heading toward IPO, not raising new funding. The category is mature. No new breakout brands raised large rounds in 2025.

- Generic lifestyle/homeware. Brands without clear category leadership or repeat economics are struggling to attract capital.

- Discount-led fashion. Brands dependent on heavy promotions without strong unit economics are being passed over.

[Internal link: Read Fastest Growing D2C Categories in India for the full market size and growth data behind each category]

The D2C IPO Pipeline: Exits That Shape D2C Funding Trends in India

IPOs are the ultimate validation for D2C funding trends in India. They prove to the ecosystem that venture-backed D2C brands can reach public-market scale.

Here is the D2C IPO landscape heading into 2026:

| Brand | IPO Status | Target Size | Key Detail |

| boAt (Imagine Marketing) | DRHP filed Oct 2025. SEBI approved. | Rs 1,500 Cr | Rs 500 Cr fresh issue + Rs 1,000 Cr OFS. Second attempt after 2022 withdrawal. |

| Honasa Consumer (Mamaearth) | Already listed (Oct 2023). | — | India’s first D2C BPC IPO. Market cap ~Rs 9,400 Cr. |

| BlueStone (Jewellery) | Listed Aug 2025. | — | Rs 1,770 Cr FY25 revenue. 200+ stores. |

| Licious (Meat/Seafood) | Deferred to 2027–28. | TBD | Prioritising profitability before listing. Rs 685 Cr FY24 revenue. |

| Curefoods | DRHP filed Sep 2025. | Rs 727 Cr fresh issue | D2C food aggregator. Owns 20+ brands including EatFit. |

The boAt IPO will be the most watched D2C listing event in 2026. If successful, it signals to the market that digital-first consumer brands can achieve public-market exits at scale. This creates a positive feedback loop for D2C funding trends in India: successful exits unlock more investor appetite for the next generation of D2C brands.

Licious’s decision to defer its IPO to 2027–28 is equally telling. The founders explicitly said they want to reach profitability before listing — rejecting the pressure to go public on hype alone. This mirrors the broader D2C funding trends in India: discipline over speed.

M&A as an Exit Path: The Rising Trend in D2C Funding

Not every D2C brand will IPO. For many, M&A (mergers and acquisitions) is the more realistic exit. And D2C funding trends in India show M&A activity rising as a complement to IPOs.

Key M&A deals that shaped the landscape:

- HUL acquired Minimalist for Rs 2,955 crore (90.5% stake) in January 2025. The largest D2C acquisition in Indian BPC history.

- Nykaa acquired Dot & Key (increased stake from 51% to 90% for Rs 265 crore in August 2024) and Earth Rhythm.

- Zydus Wellness acquired Max Protein for $46.4 million.

- Reliance Consumer Products acquired Tagz Foods for $3.3 million.

- The Souled Store acquired Redwolf to consolidate pop culture merchandise.

The signal for founders: if your brand has strong unit economics, clear category leadership, and a loyal customer base, legacy FMCG and retail companies will buy you. You do not need to build a Rs 5,000 crore business to have a successful exit. A Rs 200–500 crore D2C brand with healthy margins is an attractive acquisition target.

In 2024, there were 13 acquisitions in the Indian D2C space (per Tracxn). In 2026, Inc42 predicts M&A will be a primary channel for strategic bets by listed companies and larger conglomerates. Secondary deals and partial exits are also becoming a recognised liquidity pathway for founders and early investors.

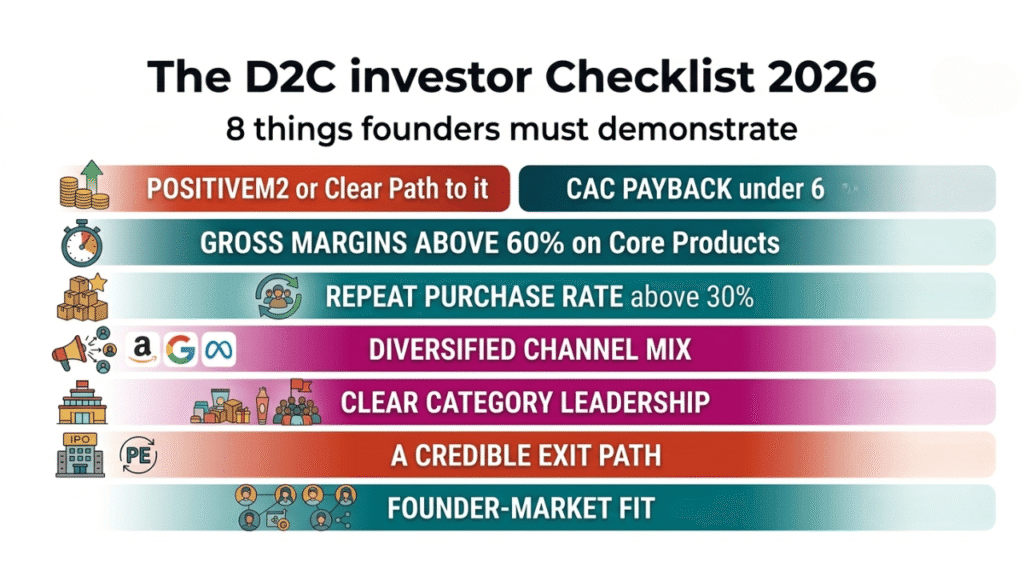

What D2C Investors Want in 2026: The New Funding Checklist

If you are a D2C founder planning to raise capital in 2026, here is the checklist investors are using. These are the D2C funding trends in India that will define who gets funded and who does not:

- Positive CM2 — or a clear path to it. Contribution margin after marketing must be positive, or provably close. Brands with negative CM2 are not getting funded. Period.

- CAC payback under 6 months. Investors want to see that each customer pays for themselves quickly. Under 3 months is excellent. Over 12 months is a red flag.

- Gross margins above 60% on core products. This is the baseline in beauty, health, and fashion. Lower margins require exceptionally strong repeat rates (like food subscriptions).

- Repeat purchase rate above 30%. Single-purchase customers destroy unit economics. Investors want proof that customers come back. A 30–40% repeat rate within 90 days signals a healthy retention engine.

- Diversified channel mix. Over-reliance on one platform (Meta, Amazon) is a risk. Investors want to see organic traffic, SEO, WhatsApp, referrals, and offline presence alongside paid ads.

- Clear category leadership. Being one of twenty skincare brands is not enough. Being the number one or number two in a specific sub-category (face serums, men’s beard care, silver jewellery) is what attracts capital.

- A credible exit path. IPO, strategic acquisition, or PE buyout. Investors need to see how they get their money back. The exit conversation is now happening at Series A, not just Series C.

- Founder-market fit. Investors are backing founders who know their category deeply. Varun Alagh’s FMCG experience at HUL and Coca-Cola. Aman Gupta’s JBL background. Domain expertise is non-negotiable.

[Internal link: Read Understanding Unit Economics for D2C Brands in India for the full cost stack investors evaluate]

Beyond VC: Alternative D2C Funding Trends in India

Not every D2C brand needs or wants venture capital. The D2C funding trends in India now include several alternatives:

Revenue-Based Financing (RBF)

Platforms like Recur Club and GetVantage offer 15–30% of monthly sales as quick-deployment capital. Repayment is tied to revenue, not fixed terms. No equity dilution. This is ideal for brands with consistent sales but who want to avoid giving up ownership.

Venture Debt

InnoVen Capital and Trifecta Capital provide venture debt that complements equity funding. It supports working capital needs (inventory, marketing spend) without dilution. boAt’s IPO filing earmarks Rs 225 crore of the fresh issue specifically for working capital — showing how cash-intensive D2C operations are even at scale.

Bootstrapping

India has nearly 11,000 D2C companies, but only about 800 have raised funding. That means the vast majority are bootstrapped. For founders in categories with strong margins (beauty, men’s grooming, wellness), bootstrapping to Rs 5–10 crore in annual revenue before raising a targeted Series A is becoming a credible strategy. It preserves equity and demonstrates real market pull.

Government Incentives

The Budget 2024 angel tax removal, reduced capital gains tax (20% → 12.5%), and PLI schemes for electronics and textiles have all reduced the structural cost of D2C investment. ONDC’s 3% commission cap offers an alternative discovery channel. These policy tailwinds support D2C funding trends in India by making the entire ecosystem more investor-friendly.

D2C Funding Outlook for 2026: What the Signals Tell Us

Based on deal flow, investor commentary, and macro signals as of early 2026, here is what D2C funding trends in India look like going forward:

- Fewer deals, but larger cheques. Investors are writing bigger cheques into fewer brands. Concentrated capital goes to proven winners. Spray-and-pray seed investing has declined sharply (seed funding down 30% in 2025 per Tracxn).

- IPOs will define the narrative. The boAt IPO is the biggest signal event. A successful listing unlocks capital recycling and investor confidence for the next generation of D2C brands. A disappointing listing dampens the entire ecosystem.

- M&A will accelerate. Legacy FMCG companies (HUL, ITC, Godrej) are actively shopping for D2C brands. Inc42 predicts M&A will be a primary exit channel in 2026. Founders should build with acquirability in mind.

- Quick commerce changes the calculus. Blinkit, Instamart, and Zepto are reshaping D2C distribution. Brands that crack quick commerce economics get a new growth lever. But it is an expensive channel — not a substitute for owned-channel profitability.

- Profitability-first is permanent. This is not a cycle. It is a structural shift. D2C funding trends in India will not return to the 2021 era of funding growth at all costs. Investors have internalised that sustainable brands need sustainable economics.

- Consumer spending tailwinds. Rising discretionary spend among the top 200 million Indian households benefits premium D2C, beauty, and convenience categories. The demand side is strong. The question is whether brands can capture it profitably.

2025 was the transition year. 2026 will be the rebalancing year. That is the thesis from Inc42 — and it captures the mood accurately. Capital is available. But it rewards discipline, not spectacle. The D2C brands that raise in 2026 will be the ones that earned it with their numbers, not their narrative.

Key Takeaways

- D2C funding in India peaked at $1.6 billion in 2022 and corrected to $757 million by 2024. The correction was not a collapse. It was a reset toward sustainable investing.

- India is the second most funded D2C market globally, behind the US. The ecosystem is alive. The rules have changed.

- Investors in 2026 demand CM2 positive, CAC payback under 6 months, gross margins above 60%, and a credible exit path. The old pitch deck of “look at our revenue growth” no longer works.

- Beauty, jewellery, food, and pet care attracted the largest D2C deals in 2025–2026. Categories with repeat consumption and strong unit economics are where capital flows.

- The boAt IPO is the most important signal event for 2026. A successful listing unlocks the next wave of D2C funding. Licious’s deferral to 2027–28 shows that smart founders prioritise readiness over speed.

- M&A is rising as a credible exit. HUL’s Rs 2,955 Cr Minimalist acquisition proves that D2C brands do not need to IPO to deliver returns.

- Alternative funding (RBF, venture debt, bootstrapping) is growing. Not every D2C brand needs VC. Founder-friendly, non-dilutive capital is increasingly available.

Frequently Asked Questions

What are the latest D2C funding trends in India?

D2C funding in India peaked at $1.6 billion in 2022, dropped to $757 million by 2024, and has stabilised in 2025–2026 at estimated similar levels. The key shift is from growth-focused investing to profitability-first investing. Investors now demand positive contribution margins, CAC payback under 6 months, and a clear exit path (IPO or M&A) before writing cheques.

How much funding did Indian D2C startups raise in 2024 and 2025?

Indian D2C startups raised $757 million in 2024 (per Tracxn), an 18% decline from $930 million in 2023. In 2025, overall Indian startup funding was approximately $10.5 billion (down 17% from 2024 per Tracxn), with D2C-specific funding estimated in the $700M–$800M range based on disclosed deals.

Which D2C categories are attracting the most funding in 2025–2026?

Beauty and skincare, jewellery, food and beverages, and pet care attracted the largest D2C rounds. Key deals include GIVA (Rs 530 Cr), The Whole Truth ($51M), Farmley ($40M), Snitch ($40M), Foxtale ($30M), and Supertails ($30M). Audio and generic lifestyle brands saw less activity.

What do D2C investors look for in 2026?

Eight factors: positive CM2, CAC payback under 6 months, 60%+ gross margins, 30%+ repeat purchase rate, diversified channel mix, clear category leadership, credible exit path (IPO or acquisition), and founder-market fit. Revenue growth alone is no longer sufficient.

Is the D2C funding winter over in India?

The acute funding winter of 2023–2024 has eased, but capital remains selective. Fewer deals are happening, but cheque sizes are larger for proven brands. IPO momentum (boAt filing, BlueStone listing) and M&A activity (Minimalist acquisition) are positive signals. The market is not back to 2021–2022 exuberance and likely never will be. It has matured into a discipline-driven ecosystem.

What are the alternatives to VC funding for D2C brands?

Revenue-based financing (Recur Club, GetVantage) offers 15–30% of monthly sales as non-dilutive capital. Venture debt (InnoVen, Trifecta) complements equity rounds. Bootstrapping to Rs 5–10 crore revenue before raising Series A preserves equity and demonstrates market pull. Government incentives (angel tax removal, PLI schemes) also reduce the structural cost of D2C investment.