The Evolution of D2C in India: Five Phases That Shaped an $80 Billion Market

From Marketplace Dependency to Digital-First Brands to Omnichannel Empires. The Full Timeline of How India Went Direct.

In 2014, if you wanted to sell a product directly to Indian consumers online, you had to build almost everything from scratch. Your own website (custom-coded, because Shopify barely existed in India). A payment integration and your own shipping network too. The cost building this system was enormous. The infrastructure was missing and the consumer was still figuring out whether it was safe to type a credit card number into a browser. This prompted the Evolution of D2C.

In 2026, a first-time founder can launch a D2C brand in a week. Shopify hosts the site, a payment gateway processes payments. Delivery partner ships the product and Checkout Apps optimise checkout. There are apps that run WhatsApp campaigns and email flows too. The entire D2C stack is plug-and-play now specially with these apps.

That gap between 2014 and 2026 is the evolution of D2C in India. It did not happen in a single moment. It happened in phases. Each phase was triggered by a specific infrastructure shift, a funding cycle, or a consumer behaviour change. Each phase produced a different kind of brand, a different set of winners, and a different set of lessons.

This article maps those five phases. Not as abstract history, but as a practical guide to understanding why the D2C market looks the way it does today, and where it is heading next.

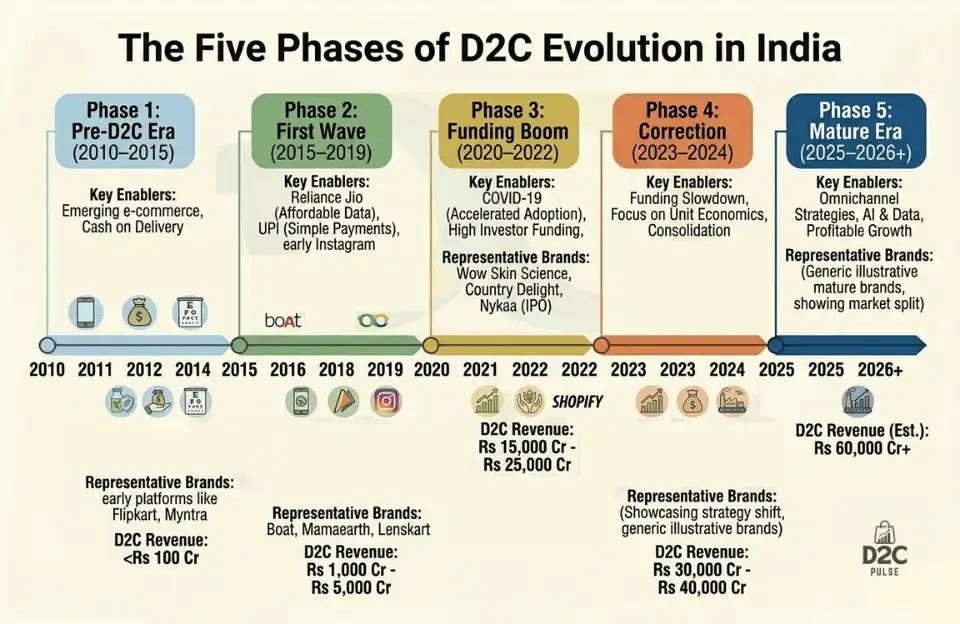

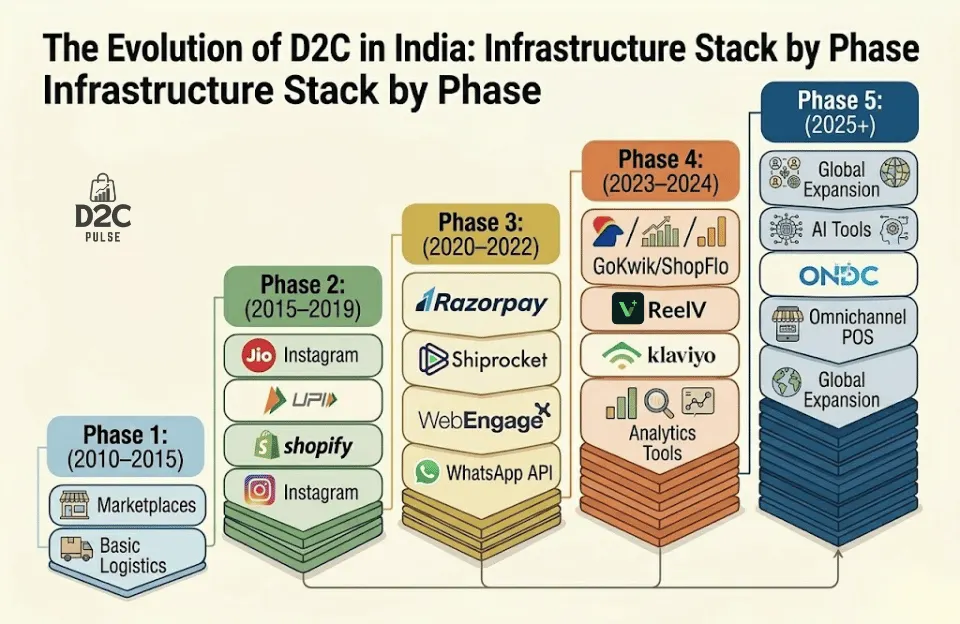

Phase 1: The Pre-D2C Era (2010–2015). When “Direct” Meant “Marketplace”

The evolution of D2C in India starts, paradoxically, with marketplaces. Between 2010 and 2015, selling online in India meant selling on Flipkart or Amazon India (which launched in 2013). These platforms built the consumer habit of buying online. They invested billions in logistics, payments, and customer trust. They trained an entire generation to shop on a screen.

During this phase, a few brands tried going direct. Lenskart launched in 2010 as an online contact lens store. Pepperfry launched in 2012 for furniture. Nykaa started in 2012 for beauty. But these were exceptions. Most brands that sold online did so through marketplaces, not their own websites.

The reason was infrastructure. Building a standalone ecommerce store in India in 2013 required custom development (Rs 5–15 lakh), manual payment gateway integration, and partnerships with individual logistics companies. There was no Shopify ecosystem, or one-click checkout and even no WhatsApp Business API. The barriers were high. Today we have both, Shopify as well as WordPress, both do not require a whole team and can be started by solopreneurs too (Maybe working with Freelance developers in case of WordPress)

What this phase did accomplish: it created the consumer base. By 2015, India had roughly 50 million online shoppers. They were concentrated in metros, were very cautious, discount-driven, and still building trust in digital commerce. But they existed, and they were growing fast.

Phase 1 of the evolution of D2C in India was not about D2C brands. It was about building the consumer habit and the logistics infrastructure that would make D2C possible later. Flipkart and Amazon spent the money. D2C brands harvested the behaviour.

Phase 2: The First Wave (2015–2019). The Founders Who Built Before the Tools Existed

Between 2015 and 2019, four things changed that made the first wave of D2C in India possible.

- Reliance Jio launched in September 2016. Mobile data prices dropped from Rs 250 per GB to Rs 10 per GB practically overnight. Internet users in India jumped from 300 million to 500 million in two years. Suddenly, the addressable market for online brands was not just metro India. It was everyone with a phone.

- UPI launched in April 2016. Digital payments became frictionless. No more entering 16-digit card numbers or waiting for net banking OTPs. A customer could pay for a product by scanning a QR code in three seconds. This reduced checkout abandonment dramatically.

- Instagram and Facebook became shopping channels. Social media advertising matured. For the first time, a founder with Rs 10,000 could run targeted ads to a specific audience in a specific city. Customer acquisition became accessible, not just to companies with TV budgets.

- Shopify entered India meaningfully. By 2017–2018, Shopify had localised its pricing and added Indian payment gateway integrations. Setting up a store dropped from a Rs 10 lakh custom project to a Rs 2,000/month subscription. The barrier to launching a D2C brand collapsed.

Also Read: Digital Infrastructure Enabling D2C in India and how is it helping develop the D2C Industry

What this led to?

This phase produced the first generation of iconic Indian D2C brands. Mamaearth (2016). boAt (2016). Sugar Cosmetics (2015). Bombay Shaving Company (2016). Sleepy Owl (2016). The Man Company (2015). Wakefit (2016). mCaffeine (2015). These founders launched with personal savings, small angel rounds, and an Instagram account. They figured out the playbook as they went.

The brands that worked during this phase shared a pattern: they found a specific gap in the Indian market (toxin-free baby care, affordable audio, bold makeup for Indian skin tones), built a strong Instagram presence, used Meta ads to acquire their first 10,000 customers, and scaled through marketplace expansion once brand pull was established.

The economics were tough with the CAC rising and return rates being high. COD orders killed cash flow, but the market was growing fast enough that these problems felt manageable.

Also Read: Key Characteristics of Successful D2C Brands in India for the traits that emerged during this phase

Phase 3: The Funding Boom (2020–2022). When COVID Poured Fuel on the Fire

Then COVID hit. And the evolution of D2C in India accelerated by five years in eighteen months.

Physical stores closed. Mall traffic went to zero. Every consumer who had never shopped online was forced to do it for the first time. Online shopping penetration spiked. D2C brands that had been growing at 30–50% year-on-year suddenly grew at 100–200%.

Investors noticed. Venture capital flooded the D2C space. In 2022 alone, Indian D2C startups raised close to $1.6 billion. Fireside Ventures, Matrix Partners, Sequoia (now Peak XV), and Tiger Global backed dozens of consumer brands. Valuations skyrocketed. Brands that were doing Rs 20 crore in revenue were valued at Rs 500 crore on the promise of future growth.

| Year | D2C Funding (est.) | Key Trend | Signature Deals |

| 2020 | ~$800M | COVID acceleration | Licious ($30M), Mamaearth ($24M), Nykaa ($100M pre-IPO) |

| 2021 | ~$1.6B | Peak funding frenzy | boAt ($100M), Mamaearth ($52M), Minimalist ($15M), Sugar ($50M), GIVA, mCaffeine |

| 2022 | ~$1.2B | Late-stage bets | Lenskart ($500M+), Country Delight ($108M), PharmEasy, Purplle |

This phase also produced 800+ new D2C brands. Everyone with a product idea and an Instagram account launched a D2C brand. The playbook felt simple: raise a seed round, spend on Meta ads, show hockey-stick growth, raise Series A and repeat.

But the economics of many Phase 3 brands were broken. CAC was growing faster than LTV. Many brands were unprofitable at the unit level, subsidising growth with VC money. The mantra was growth-at-all-costs. Profitability was a problem for later.

Later came sooner than expected.

Phase 3 of the evolution of D2C in India was defined by capital abundance and unit economics neglect. The brands that survived were the ones that used the funding to build systems (manufacturing, retention, supply chain). The ones that failed were the ones that used funding to buy customers they could not keep.

Also Read: CAC vs LTV Deep Dive for D2C Brands in India

Phase 4: The Correction (2023–2024). When the Music Stopped

In 2023, the global funding environment tightened. Interest rates rose. Tech valuations crashed. And the VC money that had been flowing into Indian D2C brands slowed to a trickle.

D2C funding in India dropped from $1.6 billion in 2022 to approximately $757 million in 2024. Fewer deals. Smaller cheques. And a new set of questions from investors: What is your contribution margin? When will you break even? What is your repeat purchase rate? Growth alone was no longer enough.

The correction was brutal for some brands. Companies that had raised at inflated valuations struggled to raise follow-on rounds. Layoffs hit the D2C sector. Brands that had never worried about profitability were suddenly fighting for survival.

But Phase 4 was not all pain. It was the phase where the evolution of D2C in India separated the operators from the opportunists.

The brands that survived the correction shared specific traits: positive contribution margins, repeat purchase rates above 25–30%, controlled ad spend (under 35% of revenue), diversified channels (not 100% dependent on Meta ads), and a clear path to profitability. Minimalist was profitable throughout. boAt turned profitable in FY25. Mamaearth had its challenges with Project Neev but recovered. Lenskart posted its first profit in FY25.

The correction also triggered a wave of exits. HUL acquired Minimalist for Rs 2,955 crore. Tata acquired Cureskin. Strategic acquirers started buying D2C brands not for growth, but for the audience, the data, and the digital capabilities they could not build in-house.

Also Read: D2C Funding Trends in India: What Investors Want in 2026 for the full funding analysis

Phase 5: The Mature Era (2025–2026). What D2C in India Looks Like Now

This is where we are today. The evolution of D2C in India has reached a phase where the model is no longer novel. It is infrastructure. The question is no longer “Should I go D2C?” It is “How do I build a profitable, scalable D2C brand in a market with 800+ competitors?”

Here is what defines Phase 5:

Omnichannel is the default, not the exception

The purely online D2C brand is becoming rare. The winning brands sell through their own website, Amazon, Flipkart, Nykaa, and physical retail. D2C brands accounted for 18% of total retail space leased in India in the first half of 2025. Lenskart has 2,700+ stores. Mamaearth has 2.36 lakh retail outlets. boAt sells in 20,000+ retail points. Online is where you start. Omnichannel is where you scale.

Unit economics are non-negotiable

Investors in 2026 require positive CM2, CAC payback under 6 months, 60%+ gross margins, and 30%+ repeat purchase rates before writing a cheque. The growth-at-all-costs era is dead. Profitability is the price of admission.

AI and automation are reshaping operations

AI-generated ad creatives cost Rs 500 instead of Rs 10,000. AI search (ChatGPT, Perplexity) is becoming a new discovery channel. Predictive analytics drive inventory and pricing decisions. Marketing automation handles WhatsApp flows, email sequences, and loyalty programs at scale. The tech cost of running a D2C brand keeps dropping.

The consumer has evolved too

India now has 345 million+ digital shoppers (projected to exceed 400 million by 2027). The majority of new shoppers come from tier-2 and tier-3 cities. They are value-conscious but brand-aware. These customers compare products on Instagram, read reviews on YouTube, and buy wherever is most convenient. Many of them are not loyal to a channel but most are loyal to brands that earn it.

Strategic exits are validating the model

The HUL-Minimalist deal (Rs 2,955 crore), the Lenskart IPO filing ($10 billion target), and the boAt IPO filing are proof that building a D2C brand in India can lead to real, large-scale outcomes. The exit path is no longer hypothetical.

The Five Phases of the Evolution of D2C in India: Summary

| Phase | Period | Key Enabler | Defining Trait | Representative Brands |

| 1. Pre-D2C | 2010–2015 | Flipkart, Amazon India build online shopping habit | Marketplace dependency. Few direct brands. | Lenskart, Nykaa, Pepperfry (early) |

| 2. First Wave | 2015–2019 | Jio, UPI, Instagram ads, Shopify | Digital-first brands. Instagram-led growth. Founder-driven. | Mamaearth, boAt, Sugar, Wakefit, mCaffeine |

| 3. Funding Boom | 2020–2022 | COVID acceleration. $1.6B peak funding. | Growth-at-all-costs. 800+ brands launched. Valuations soar. | Minimalist, Licious, Country Delight, The Whole Truth |

| 4. Correction | 2023–2024 | Funding winter. Rising interest rates. | Unit economics focus. Layoffs. M&A exits. Survivors emerge. | Minimalist (HUL exit), boAt (profitable), Mamaearth (IPO) |

| 5. Mature Era | 2025–2026+ | Omnichannel. AI. Strategic exits. | Profitability required. Omnichannel default. Global expansion. | Lenskart (IPO), GIVA, Foxtale, Snitch, Supertails |

What Comes Next: Phase 6 of the Evolution of D2C in India

The evolution of D2C in India is not complete. Here are five trends shaping the next phase.

- AI-native brands. The next generation of D2C brands will use AI not just for marketing, but for product development (formulation optimisation), demand forecasting (inventory management), and customer service (conversational commerce). The cost of running a D2C operation will drop further.

- ONDC as a distribution layer. The Open Network for Digital Commerce lets brands sell through an interoperable network with commissions around 3%, compared to 15–25% on Amazon. Over 700,000 vendors have joined. As consumer adoption grows, ONDC will become a real alternative to marketplace dependency.

- International expansion. Lenskart is in Japan, Singapore, and the UAE. Minimalist is expanding globally through HUL. Mamaearth has entered the US and Southeast Asia. Indian D2C brands are going global, not just serving India. The next five years will see more $100M+ revenue Indian D2C brands with significant international business.

- Consolidation through M&A. Large FMCG companies (HUL, ITC, Tata Consumer) will continue acquiring D2C brands to access digital-first audiences and capabilities. D2C brands that build strong, differentiated positions become attractive acquisition targets.

- Tier-2 and tier-3 as the growth frontier. Over 60% of new D2C customers come from smaller cities. Brands that can adapt their pricing, messaging, and distribution for non-metro India will capture the next wave of growth. The D2C playbook written for Bangalore and Mumbai does not automatically work in Lucknow and Indore. The brands that figure this out will define Phase 6.

Key Takeaways

- The evolution of D2C in India has five distinct phases: Pre-D2C (2010–2015), First Wave (2015–2019), Funding Boom (2020–2022), Correction (2023–2024), and the Mature Era (2025–2026+). Each was triggered by specific infrastructure, funding, and consumer shifts.

- Infrastructure enabled each phase. Jio and UPI enabled Phase 2. COVID and VC capital enabled Phase 3. AI and omnichannel tools are enabling Phase 5. The brands did not create the wave. The infrastructure did.

- Growth-at-all-costs died in Phase 4. The correction of 2023–2024 killed the playbook of burning VC money on unprofitable customer acquisition. Unit economics are now the price of admission.

- Omnichannel is the mature D2C model. Starting online and staying online-only is a Phase 2 strategy. Phase 5 brands sell everywhere: own website, marketplaces, physical stores, quick commerce.

- India is now the world’s third-largest D2C market. 800+ D2C brands, $80 billion+ addressable market, 345 million digital shoppers. The evolution of D2C in India is no longer early-stage. It is a structural shift in how Indians buy.

- Strategic exits prove the model works. Minimalist (Rs 2,955 Cr acquisition), Lenskart ($10B IPO target), boAt (IPO filing). Building a D2C brand in India can produce real, large-scale outcomes.

Frequently Asked Questions

What are the phases of the evolution of D2C in India?

The evolution of D2C in India has five phases: (1) Pre-D2C Era (2010–2015) when marketplaces built the online shopping habit, (2) First Wave (2015–2019) when Jio, UPI, and Shopify enabled the first digital-first brands, (3) Funding Boom (2020–2022) when COVID and VC capital supercharged growth, (4) Correction (2023–2024) when the funding winter forced unit economics discipline, and (5) Mature Era (2025–2026+) when omnichannel, profitability, and strategic exits became the norm.

How big is the D2C market in India?

India’s D2C addressable market is estimated at over $80 billion as of 2024, making it the third-largest D2C market globally after the US and China. India has 800+ D2C brands, 345 million+ digital shoppers, and the market is projected to grow at a 24% CAGR through 2030.

What enabled the growth of D2C in India?

Four infrastructure shifts enabled D2C growth: Reliance Jio (2016) brought cheap mobile data to 500 million users, UPI (2016) made digital payments frictionless, Shopify and SaaS tools lowered the cost of launching a store, and Meta’s advertising platform made customer acquisition accessible to small brands. COVID (2020) then accelerated adoption by forcing consumers online.

What is Phase 5 of D2C in India?

Phase 5 (2025–2026) is the mature era. Omnichannel is the default. Unit economics are non-negotiable. AI is reshaping operations. Strategic exits (acquisitions and IPOs) are validating the model. The consumer has evolved to 345 million+ digital shoppers, with tier-2 and tier-3 cities driving growth. Building a D2C brand in India is no longer novel. It is a proven model with established playbooks.