How Tier-2 and Tier-3 India Is Becoming the Real D2C Battleground

60% of New D2C Customers Come from Smaller Cities. Here Is Who They Are, How They Buy, What They Expect, and How to Reach Them.

Ask most D2C founders where their customers are, and they will say Mumbai, Bangalore, Delhi, Hyderabad. While over 60% of new D2C customers in India now come from outside the top 8 metro cities. Regional D2C growth of ecommerce is expanding at 23% annually, projected to reach Rs 8.3 lakh crore by 2026. Over 60% of all ecommerce transactions in India now originate from tier-2 and tier-3 markets. Tier-3 cities posted a 77% surge in digital payments for watches and jewellery in 2025. D2C beauty brands saw a 70% revenue increase specifically from tier-3 cities like Guwahati and Rajkot.

These are not emerging markets any more, they are the market. Regional D2C growth beyond metros is not just a trend line in a market report. It is a structural shift in where Indian commerce is heading. The consumer in Indore, Coimbatore, Lucknow, and Jaipur is digitally fluent, brand-aware, and ready to buy directly from brands. But they are not the same consumer as the one in Mumbai. They have different price expectations, different payment preferences, different language defaults, and different trust signals. The D2C playbook that works in Bangalore does not automatically work in Bhopal.

This guide covers who the non-metro D2C consumer is, which cities are driving the growth, what operational challenges brands face when expanding beyond metros, and the eight-step playbook for capturing this market.

The Numbers Behind Regional D2C Growth Beyond Metros

| Metric | Data Point |

| New D2C customers from non-metro cities | 60%+ (2025) |

| Tier-2/3 ecommerce growth rate | 23% annually, reaching Rs 8.3 lakh crore by 2026 |

| Share of ecommerce transactions from tier-2/3 | 60%+ of all India ecommerce (2025) |

| Internet users in rural India | 57% of total active users (548M+), growing 4x faster than urban |

| UPI adoption in non-metro markets | 67% of consumers use UPI as default payment |

| Tier-3 digital payment surge (watches/jewellery) | 77% increase in 2025 |

| Tier-2 digital payment surge (grocery) | 46% increase in 2025 |

| D2C beauty revenue growth from tier-3 | 70% increase from cities like Guwahati, Rajkot (2025) |

| SUGAR Cosmetics sales from non-metros | 60%+ from cities like Siliguri, Karnal, Bhatinda |

| Projected online shoppers from tier-2/3 by 2030 | 88% of new online shoppers (RedSeer) |

The data is unambiguous. Regional D2C growth beyond metros is not a secondary opportunity. It is the primary growth vector for the next five years. The brands that figure out how to serve these consumers will capture the majority of India’s D2C expansion.

[Internal link: Read The Evolution of D2C in India for how this shift fits into the broader market timeline]

Who Is the Non-Metro D2C Consumer? A Profile That Metro Founders Get Wrong

Most metro-based founders make a predictable mistake. They assume the tier-2 consumer is a cheaper version of the metro consumer. Same preferences. Lower budget. That is wrong. The non-metro D2C consumer is a different buyer with different decision-making patterns.

They are aspirational but value-calculating

The tier-2 consumer wants branded products. They have seen them on Instagram. They want what Mumbai has. But they calculate value differently. They are not looking for the cheapest option. They are looking for the best product within a mental price range. A Rs 1,200 serum is fine if they understand why it costs Rs 1,200. A Rs 1,200 serum with no explanation feels like a risk. Education and justification matter more in non-metros because these consumers are often spending on a D2C brand for the first time.

They discover through video, not search

The metro consumer discovers products through Google Search and Instagram ads. The non-metro consumer discovers through YouTube and Instagram Reels. Their primary internet experience is video, not text. They watch product demos, unboxing videos, and creator reviews before they buy. A brand that only invests in search ads and text-heavy product pages is invisible to this consumer.

They trust people, not platforms

In metros, consumers trust Amazon reviews and branded websites. In tier-2 and tier-3, they trust a neighbour’s WhatsApp recommendation, a regional creator’s review, or a micro-influencer they follow. 80% of social commerce buyers cite peer influence. This is even stronger in non-metros. A recommendation from a relatable local voice carries more weight than a polished brand campaign.

They still prefer COD, but UPI is catching up

Cash-on-delivery remains dominant in non-metros, accounting for up to 70% of orders in some regions. But UPI adoption has reached 67% as the default payment method. The shift is happening fast. Smart D2C brands offer both, with WhatsApp-based COD-to-prepaid nudges that convert 10–20% of COD orders to online payment after the order is placed.

They shop in their language

The non-metro consumer processes information faster in Hindi, Tamil, Telugu, Marathi, or Bengali than in English. Regional language ads deliver 2.5x higher CTR in these markets. Product videos in the local language convert 2–3x better than English-only content. Brands that localise their ads, WhatsApp messages, and product page videos unlock a consumer segment that English-only brands cannot access.

The non-metro D2C consumer is not a discount shopper. They are a first-time buyer of branded products who needs education, video, trust signals, vernacular communication, and a price point that feels fair. The brands that treat them as a lesser version of the metro consumer will fail. The brands that build for them specifically will capture the next decade of D2C growth in India.

Which Cities Are Driving Regional D2C Growth Beyond Metros?

Not all non-metro cities are equal. Some are growing faster than others. Here is where the action is concentrated.

| City | Tier | Why It Matters for D2C | Notable Signal |

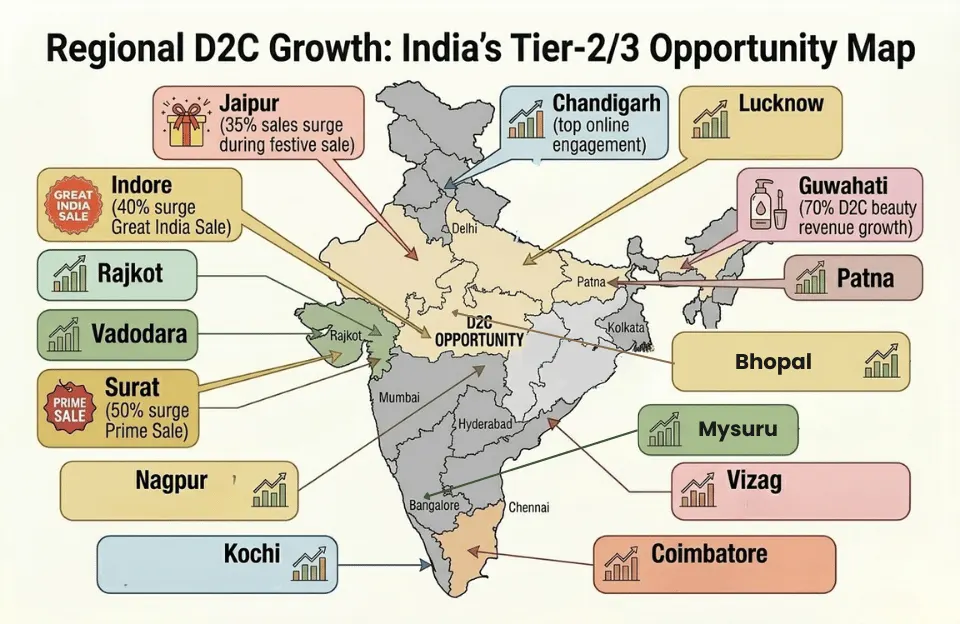

| Jaipur | Tier 2 | D2C brand hub (Minimalist, Freewill HQ). Growing consumer base. | 35% online sales surge during festive season. |

| Indore | Tier 2 | Fast smartphone adoption. Price-sensitive but aspirational. | 40% surge during Great India Sale. |

| Surat | Tier 2 | Textile and manufacturing hub. High ecommerce adoption. | 50% surge during Prime Sale. |

| Coimbatore | Tier 2 | Top online shopping engagement. Strong disposable income. | Habanero Foods reports hottest demand from Coimbatore. |

| Lucknow | Tier 2 | Large population. Leading online shopping engagement. | Growing D2C beauty and fashion hub. |

| Chandigarh | Tier 2 | High disposable income. Early digital adopter. | LetsShave HQ. Premium D2C demand. |

| Guwahati | Tier 3 | Northeast gateway. Underserved by traditional retail. | 70% D2C beauty revenue growth. |

| Vizag | Tier 2 | Growing tech and consumer base in AP. | Habanero Foods fast-growing order source. |

| Nagpur | Tier 2 | Central India logistics hub. Growing online adoption. | Strong COD-to-UPI transition underway. |

| Rajkot | Tier 3 | Gujarat’s second city. Rising D2C demand. | 70% D2C beauty revenue growth alongside Guwahati. |

The pattern is clear. Tier-2 cities like Jaipur, Indore, Surat, Coimbatore, and Lucknow are already generating significant D2C volume. Tier-3 cities like Guwahati, Rajkot, and Mysuru are growing even faster because they are underserved by both traditional retail and D2C brands. The earlier a brand enters a tier-3 city, the stronger its position becomes. First movers in these markets face less competition and build loyalty with consumers who are buying from a D2C brand for the first time.

The Operational Challenges of Regional D2C Growth Beyond Metros

Selling to tier-2 and tier-3 is not just a marketing problem. It is an operations problem. Here are the five biggest challenges.

Challenge 1: Logistics and last-mile delivery

Metro delivery takes 1–2 days. Tier-2 takes 2–4 days. Tier-3 and beyond can take 5–7 days. Last-mile delivery infrastructure in smaller cities is still developing. Shiprocket covers 24,000+ PIN codes, but delivery times and reliability are uneven. Every extra day of delivery time reduces the chance of repeat purchase. Brands expanding beyond metros need regional warehouse strategies or fulfilment hubs in cities like Jaipur, Indore, and Lucknow to cut delivery times.

Challenge 2: High COD rates and RTO

COD dominates non-metro orders at up to 70%. COD orders have higher return-to-origin (RTO) rates because the customer has not pre-committed financially. RTO rates of 25–30% are common. Each returned order costs the brand forward shipping + reverse shipping + product damage risk. Smart brands use WhatsApp nudges post-order to convert COD to prepaid (offering a small discount or free add-on). This alone can convert 10–20% of COD orders and reduce RTO.

Challenge 3: Language and communication

English-first communication creates a barrier. Product pages, ads, WhatsApp messages, and customer support in English work in metros. In Lucknow, Patna, or Guwahati, they create friction. Brands need vernacular ad creatives, Hindi or regional language WhatsApp flows, and ideally product videos in the local language. This is not a translation exercise. It is a cultural adaptation exercise. The tone, the references, and the examples must feel local.

Challenge 4: Price sensitivity and entry-point pricing

The average order value (AOV) in tier-2/3 is typically 20–40% lower than in metros. A Rs 2,500 product that sells well in Mumbai may need a Rs 799 starter kit or a Rs 499 mini version to gain entry in Indore. Sachetisation (small-size trial packs) is not a compromise. It is a strategy. Mamaearth’s trial kits, Minimalist’s smaller serum sizes, and boAt’s sub-Rs 500 earbuds all serve as entry points for non-metro consumers.

Challenge 5: Building trust without physical presence

In metros, consumers are comfortable buying from a website they have never visited in person. In tier-2/3, trust takes longer to build. The consumer may have never heard of your brand. They are used to buying from local shops where they can touch the product and return it face-to-face. D2C brands expanding beyond metros need to invest in trust signals: shoppable videos showing real product use, creator testimonials from relatable regional voices, strong return policies, and WhatsApp support that feels personal.

Regional D2C growth beyond metros is an operations challenge as much as a marketing challenge. The brand that solves delivery speed, COD conversion, vernacular communication, entry-point pricing, and trust for non-metro consumers will capture the largest share of India’s D2C expansion.

[Internal link: Read How to Reduce CAC for D2C Brands for specific tactics including regional language ads and CTWA campaigns]

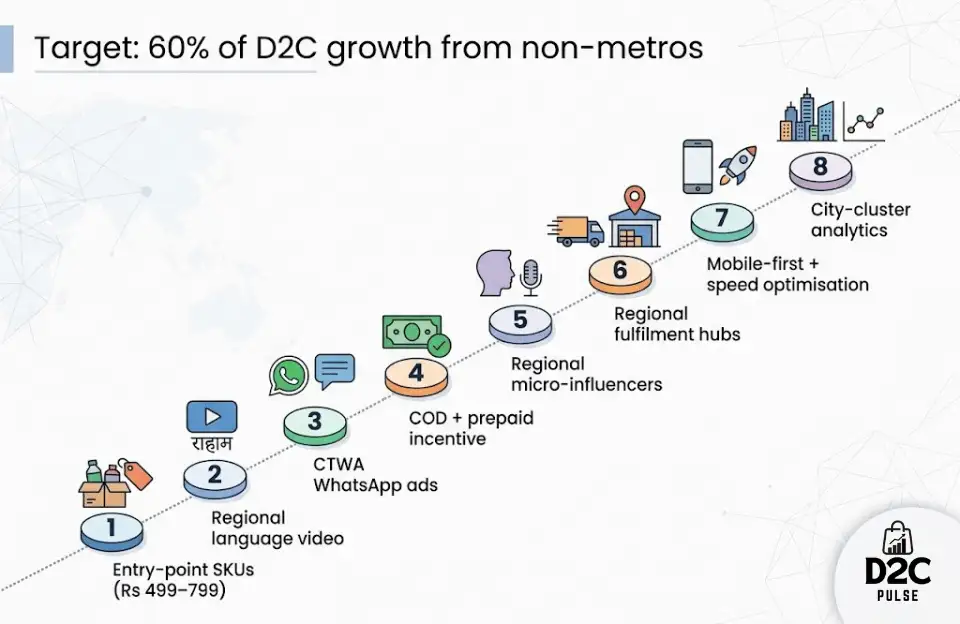

The Eight-Step Playbook for Capturing Regional D2C Growth Beyond Metros

- Create entry-point SKUs specifically for non-metro markets. A Rs 499–799 trial size or starter kit with free shipping. This is the first transaction and goal here is not profit. It is to convert a first-time buyer into a repeat customer. If the product is good, the second and third orders will be at full price.

- Produce video content in regional languages. Hindi as a baseline, then add Tamil, Telugu, Marathi, and Bengali based on your target cities. Product demos, founder stories, and customer testimonials in the local language convert 2–3x better. Use shoppable video tools like ReelV to place these directly on product pages so the non-metro consumer sees relevant content at the point of purchase.

- Run Click-to-WhatsApp ads targeting tier-2/3 cities. CTWA ads reduce CAC by 25–40% versus click-to-website ads. The WhatsApp conversation builds trust, answers questions, and closes the sale. The phone number you collect becomes your retention channel. This is the single most effective acquisition channel for non-metro consumers who want to ask before they buy.

- Offer COD with a prepaid incentive. Do not remove COD as it’s essential to the non-metro consumer. But add a WhatsApp message after order placement offering Rs 50 off or a free sample if they switch to online payment or partial payment. This converts 10–20% of COD orders and reduces your RTO risk.

- Partner with regional micro-influencers. A skincare creator in Jaipur with 30,000 followers has more purchase influence in that market than a Mumbai celebrity with 5 million. Regional creators feel relatable. Their recommendations carry trust. Budget Rs 5,000–15,000 per creator for authentic product reviews. Scale to 20–50 creators across target cities.

- Set up regional fulfilment hubs. A warehouse in Jaipur, Nagpur, or Lucknow cuts delivery time to surrounding tier-2/3 cities from 5–7 days to 2–3 days. Faster delivery increases repeat rates and reduces COD cancellations. Shiprocket and Delhivery both offer multi-city fulfilment options.

- Adapt your product pages for mobile and speed. 70% of non-metro shopping happens on mobile phones on variable network speeds. If your product page takes more than 3 seconds to load on a 4G connection, you lose the consumer before they see the product. Optimise images, use lightweight page designs. If you use shoppable videos, choose tools like ReelV that run on separate CDN infrastructure so video does not slow down the page.

- Track unit economics by city cluster, not just by channel. Your CAC in Jaipur is different from your CAC in Mumbai and your AOV in Coimbatore is different from your AOV in Delhi. The RTO rates in Lucknow are different from the RTO rates in Bangalore. Segment your analytics by city cluster and optimise separately for each market. Brands that treat all of India as one market overspend in metros and underinvest in the cities where growth is actually happening.

Indian D2C Brands Winning in Non-Metro Markets

- SUGAR Cosmetics: Over 60% of sales from non-metro cities like Siliguri, Karnal, and Bhatinda. Bold, affordable makeup with strong Instagram and influencer presence that resonates beyond metros.

- Lenskart: 2,067 stores in India, with aggressive tier-2/3 expansion. Franchise model (FOFO) enables fast entry into smaller cities. Eye tests and physical try-on solve the trust problem for non-metro first-time buyers.

- GIVA: 240+ physical stores with expansion targeting tier-2 cities specifically. Silver and lab-grown diamond jewellery at accessible price points. Rs 530 crore Series C funding backs the offline expansion.

- ClearDekho: Built its entire model around affordable eyewear for tier-3 and tier-4 towns. Where Lenskart targets tier-2, ClearDekho targets the next layer down.

- Habanero Foods: Founder reports that Coimbatore, Vizag, Indore, and Mysuru now generate orders faster than metros. Local warehousing planned to cut delivery times for smaller cities.

- Meesho: 35% of India’s social commerce market. Built specifically for non-metro micro-entrepreneurs. Vernacular onboarding. Zero-commission model. Reaches PIN codes that D2C websites never will.

Key Takeaways about Regional D2C Growth

- 60%+ of new D2C customers come from outside the top 8 metros. Regional D2C growth beyond metros is the primary growth vector for the next five years. Not a side market. The main market.

- The non-metro consumer is different. Aspirational but value-calculating. Video-native, not search-native. Trusts people over platforms. Prefers COD but adopting UPI fast. Shops in their regional language.

- Tier-2/3 ecommerce is expanding at 23% annually. Cities like Jaipur, Indore, Surat, Coimbatore, and Lucknow are already generating significant D2C volume. Tier-3 cities like Guwahati and Rajkot are growing even faster.

- Five operational challenges define non-metro expansion: logistics speed, high COD rates, language barriers, price sensitivity, and trust deficit. Each must be solved operationally, not just with better ads.

- The 8-step playbook: entry-point SKUs, regional language video, CTWA WhatsApp ads, COD with prepaid incentive, regional micro-influencers, regional fulfilment hubs, mobile-first pages, and city-cluster analytics.

- Vernacular video is the unlock. Regional language product videos convert 2–3x better than English-only content. Place them on your product pages via shoppable video tools for maximum impact at the point of purchase.

- The D2C playbook written for Mumbai does not work in Indore. Adapt pricing, language, payment options, trust signals, and fulfilment for each city cluster. Brands that treat India as one market overspend where growth is not and underinvest where it is.

Frequently Asked Questions about Regional D2C Growth

How important is regional D2C growth beyond metros for Indian brands?

Regional D2C growth beyond metros is now the primary growth driver for Indian D2C brands. Over 60% of new D2C customers come from tier-2 and tier-3 cities. Ecommerce in these markets is growing at 23% annually. By 2030, RedSeer projects that 88% of new online shoppers will come from non-metro India. Brands that do not build for these consumers will miss the majority of D2C growth.

Which Indian cities are driving D2C growth outside metros?

The top tier-2 cities driving D2C growth are Jaipur, Indore, Surat, Coimbatore, Lucknow, Chandigarh, Vizag, and Nagpur. Tier-3 cities like Guwahati, Rajkot, Mysuru, Patna, and Vadodara are growing even faster because they are underserved by both traditional retail and existing D2C brands. First movers in these cities face less competition and higher customer loyalty.

What are the main challenges of selling D2C in tier-2 and tier-3 cities?

The five main challenges are: slower last-mile delivery (3–7 days vs 1–2 days in metros), high COD rates (up to 70%) with higher RTO, language barriers (English-first communication creates friction), lower average order values (20–40% below metro), and trust deficit (consumers are often buying from a D2C brand for the first time and need more reassurance).

How should D2C brands adapt their pricing for non-metro markets?

Create entry-point SKUs at Rs 499–799 (trial sizes, starter kits, mini versions). The goal of the first order is not profit. It is to convert a new consumer into a repeat customer. Once trust is built, the second and third orders can be at full price. Sachetisation and bundle pricing work well in non-metro markets.